Value Investing News

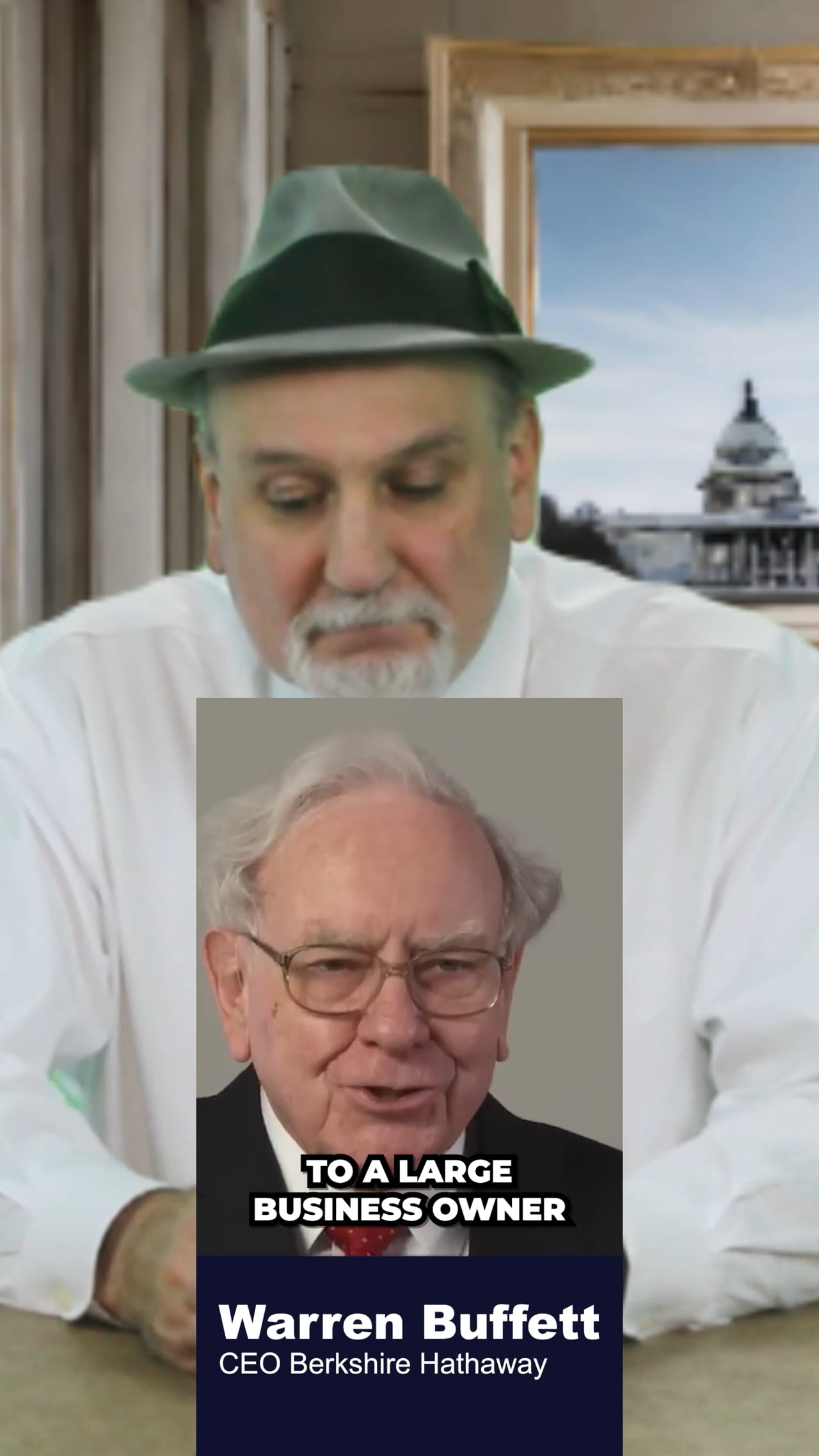

Customer First: Warren Buffett's Business Philosophy

In this enlightening video short, delve into the wisdom of Warren Buffett as he underscores the paramount importance of delighting customers.

Buffett recommends prioritizing customer satisfaction which fosters long-term success in business. All business owners should follow Buffett's timeless advice: prioritize the customer, consistently deliver value, and cultivate enduring relationships built on trust and satisfaction.

Third Avenue Value Fund Q1 2024 Portfolio Manager Commentary

For the three months ended March 31, 2024, the Third Avenue Value Fund returned 8.58%, as compared to the MSCI World Index, ...

How Loud Budgeting Can Boost Your Investing Success

Loud budgeting is one of the latest TikTok finance trends. Does it hold merit to improving one’s investing success? Read our ...

11 of the Best Investing Books for Beginners

Here are 11 of the best investing books for beginners: long-term investing Berkshire Hathaway Inc. BRK.A BRK.B "The Little ...

2 Warren Buffett Stocks You Can Buy With This Year's Average $3,011 Tax Refund

Investors can find Buffett-owned stocks without leaving the consumer sector. Another tax day has come and gone, and refunds ...

How Much Will Warren Buffett’s Will Leaves His Kids? It’s Less Than You Might Expect

Warren Buffett, chair of Berkshire Hathaway and one of the most famous investors, has made his estate plan known for a while.

3 Warren Buffett Stocks to Buy Now: Q2 Edition

InvestorPlace - Stock Market News, Stock Advice & Trading Tips Warren Buffett is one of the most successful investors of all ...

Billionaires Warren Buffett and Ken Griffin Both Own This Vanguard ETF. Should You?

Warren Buffett and Ken Griffin stand out as two of the most prominent billionaire investors on the planet. Buffett has led ...

Warren Buffett Predicts ‘Bad Ending’ for Bitcoin — Is It a Doomed Investment?

Currently sitting in sixth on Forbes' Real-Time Billionaires List, Berkshire Hathaway co-founder, chairman and CEO Warren ...

12 Warren Buffett Quotes Every 30-Year-Old Needs To Hear

In our teens and twenties, most of us want to do things our own way. But by the time we reach our 30s, the realities of life ...

Warren Buffett Is Averaging Over $2.7 Million Per Day From This Dividend Stock - Should You Load Up?

With a forward dividend rate of $0.96 per share, Berkshire Hathaway is set to receive a staggering $991,537,925.76 in annual ...

Fact Check: Fox News video of Warren Buffett promoting bitcoin giveaway is a deepfake

A video of a Fox News broadcast showing American billionaire investor Warren Buffett promoting a bitcoin giveaway is fake, ...

3 Warren Buffett Dividend Stocks Analysts Predict Will Grow By As Much As 19%

Warren Buffett, with a formidable net worth exceeding $130 billion, remains a titan of investment. His acumen for selecting ...

11 Best Coal Mining Stocks To Invest In

In this piece, we will take a look at the 11 best coal mining stocks to invest in. To know more about the top stocks, go directly to 5 Best Coal Mining Stocks To Invest In. Coal has been ...

11 Best Coal Mining Stocks To Invest In

Insider Monkey’s Q4 database results show that Alpha Metallurgical Resources, Inc. (NYSE:AMR) held 20 hedge funds out of 933 funds with Mohnish Pabrai as the largest stakeholder with 394,313 ...

With no savings at 40, I’d listen to billionaire Warren Buffett and build wealth

Investing legend Warren Buffett is well worth learning from, whether by an investor who is just starting out or who has been ...

'I am playing in extra innings': Warren Buffett gets real about death — his own and Charlie Munger's — and how his children plan to execute his will. Here are 3 estate t…

“At 93 [years old], I feel good but fully realize I am playing in extra innings,” he stated in the letter, published Nov. 21.

Warren Buffett Says Buying Gold Is 'Going Long On Fear,' But Robert Kiyosaki Says 'F U Buffett' And Urges 'Buy More Gold' — Who's Right?

The same year, in a CNBC "Squawk Box" interview, Buffett described investing in gold as “a way of going long on fear,” ...

How To Invest Like Warren Buffett in 2024

Marc is a freelance contributor to Newsweek’s investing team. He is a Certified Personal Finance Counselor and a frequent runner who aims to complete more than 100 marathons in his lifetime.

Warren Buffett has left the table. Homeless charity asks investors to bid on meal with software CEO

The California homeless charity that received $53 million over the years from investors who wanted a private lunch with billionaire Warren Buffett has found a new business executive to auction off ...